Staying informed about changes in tax regulations and family dynamics can help you make informed decisions and adapt your estate plan accordingly to reflect your evolving circumstances and priorities.

Estate planning is the essential process of organizing how your possessions will be distributed and administered after your death. To guarantee that your objectives are properly carried out, it is imperative that you comprehend estate planning regulations. This beginner’s guide will explore five key points to help you navigate estate planning laws with confidence.

1. Define Your Objectives:

Setting goals is the first step in developing an effective estate plan. Begin by evaluating your present financial circumstances, taking into account your obligations, assets, and sources of income. Next, consider your family’s dynamics, including your partner, kids, and any dependents, and how you would like to support them in the event that you become incapacitated or die. Take into account any humanitarian objectives or charity ambitions you may have as well. You may ensure that your intentions are carried out as per your specifications by defining your objectives clearly and customizing your estate plan to suit your beliefs, priorities, and aspirations.

2. Familiarize Yourself with Legal Terminology:

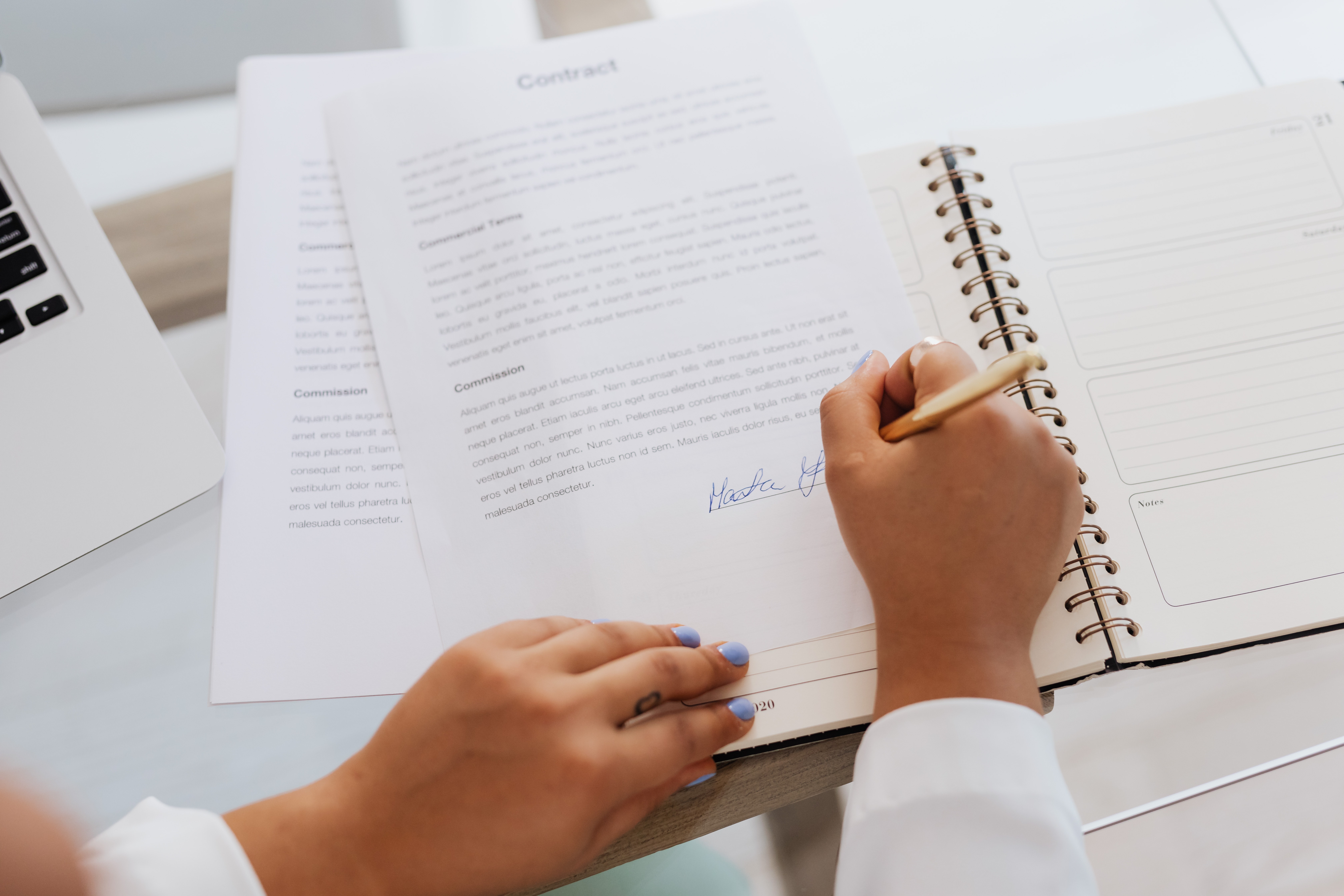

To properly navigate the estate planning process, one must be familiar with legal jargon. Begin by learning the common words used in estate planning talks and paperwork through research. One collection of legal documents that specify how you want your possessions to be allocated when you pass away is a will. A trustee, or third party, is authorized by law to retain assets on behalf of beneficiaries under a trust. If you are unable to act for yourself in court, someone else has the authority to do so on your behalf thanks to a power of attorney. In contrast, probate refers to the court-supervised process of distributing a deceased person’s inheritance. A person or organization that qualifies to receive estate assets is known as a beneficiary. You may interact with attorneys more skillfully and decide on your estate plan with more knowledge if you are aware of these phrases and their meanings.

3. Understand State-Specific Laws:

Understanding the intricacies of the state-specific legislation guiding the process is essential while exploring estate planning. It is crucial to get advice from an experienced legal expert since estate planning regulations in each state may differ greatly from those in other states. For instance, a California estate planning law firm would need to navigate laws unique to that state, such as community property regulations and Proposition 13 considerations, which may not apply in other jurisdictions. Through the assistance of skilled attorneys knowledgeable in state-specific estate planning laws, people may make sure that their estate plans are carefully written to comply with local laws and efficiently protect their assets and wishes going forward.

4. Navigating Estate Taxes:

Estate taxes, imposed upon property transfer after death, are contingent upon the total value of the estate and relevant tax laws. Effective estate planning can lessen these taxes through various strategies. By gifting assets during one’s lifetime, establishing trusts, and utilizing tax exemptions and deductions, individuals can reduce their tax burden. Gifting allows for tax-free transfer of assets up to a certain limit, while trusts help assets bypass probate and potentially decrease taxable estate value. Furthermore, individuals can take advantage of various tax deductions and exemptions provided by law to enhance tax efficiency. These strategies enable estate planners to preserve more assets for beneficiaries and mitigate the impact of estate taxes on their legacy.

5. Review and Update Your Plan Regularly:

Maintaining the efficacy and applicability of your estate plan over time requires regular reviews and updates. Your estate plan may need to be adjusted as a result of changes in life events, financial conditions, and legal requirements. Make time to examine your strategy with your financial planner or legal counsel at least once a year. Major life events like marriage, divorce, having children or adopting them, changes in health, or notable adjustments to assets or responsibilities should all be taken into account during periodic evaluations. Keep yourself updated on any modifications to estate planning rules and regulations that could have an impact on your strategy. You may make sure that your estate plan still appropriately reflects your preferences and protects your loved ones by updating it.

Conclusion:

By defining your objectives, familiarizing yourself with legal terminology, understanding state-specific laws, consulting with legal professionals, and reviewing your plan regularly, you can navigate estate planning laws effectively and ensure that your assets are managed and distributed according to your wishes. Staying informed about changes in tax regulations and family dynamics can help you make informed decisions and adapt your estate plan accordingly to reflect your evolving circumstances and priorities.

Join the conversation!